Alright, let’s talk about one of the most insidious, frustrating, and potentially expensive tax traps for active traders: the wash sale rule. If you don’t understand this rule, you could end up with a shocking tax bill, even in a year where you lost money trading. 🤯

Sounds crazy, right? But it happens all the time. Our team has seen countless developing traders get blindsided by this because they simply didn’t know the wash sale rule existed or how it worked.

Here’s the deal: The IRS has specific rules designed to prevent investors from creating artificial tax losses. While the intention might be sound, the wash sale rule, as written, is a nightmare for anyone who trades frequently. In this guide, we’ll break down exactly what the wash sale rule is, how it functions mechanically, the common traps it sets (especially the dreaded IRA trap!), and the strategies you can use to navigate or completely eliminate its impact.

What is the Wash Sale Rule? (IRS Definition)

According to the IRS (specifically in Publication 550), a wash sale occurs when you sell or trade securities at a loss and, within 30 days before or after the sale, you do one of the following:

- Buy substantially identical securities.

- Acquire substantially identical securities in a fully taxable trade.

- Acquire a contract or option to buy substantially identical securities.

If you trigger this rule, the IRS disallows your loss deduction for that sale in the current tax year.

Why the Rule Exists: Preventing Artificial Tax Losses

The IRS created the wash sale rule to stop taxpayers from “harvesting” losses for tax benefits without actually changing their economic position. Imagine selling a stock for a $1,000 loss on December 30th to reduce your taxes, only to buy it right back on January 2nd. You haven’t really exited the position, so the IRS says you can’t claim that loss yet.

How the Wash Sale Rule Works: The Mechanics

Understanding the moving parts is key to avoiding the trap.

The Core Trigger: Selling at a Loss

The rule only applies when you sell a security for less than you bought it for. Selling for a profit never triggers a wash sale.

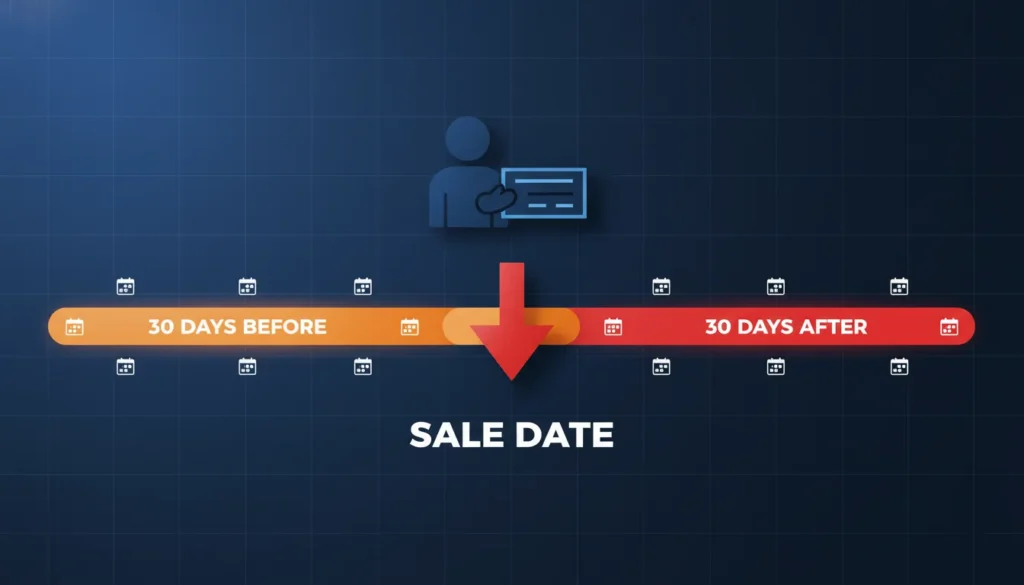

The 61-Day Window (30 Days Before + Sale Date + 30 Days After)

This is where most people get confused. The “30-day rule” isn’t just 30 days after you sell. It’s a 61-day window centered around the date of your loss sale:

- 30 days BEFORE the sale: If you buy shares before selling at a loss, those new shares can trigger the rule.

- The Day OF the sale: The date you realize the loss.

- 30 days AFTER the sale: If you buy shares after selling at a loss, those new shares trigger the rule.

If you acquire substantially identical securities anywhere within this 61-day period, the loss on the sale is disallowed.

The Consequence: Loss Disallowed

The immediate impact is simple: you cannot deduct the loss on your tax return for the year of the sale. It doesn’t just disappear, though.

The Cost Basis Adjustment: How the Loss Carries Forward

Instead of vanishing, the disallowed loss is added to the cost basis of the replacement shares (the ones you bought within the 61-day window). This effectively defers the tax benefit of the loss until you sell the new shares (and don’t trigger another wash sale).

A Clear Example of the Wash Sale Calculation

Let’s use our hypothetical XYZ stock data:

- June 1st: Buy 100 shares of XYZ @ $50/share (Cost Basis = $5,000).

- July 10th: Sell 100 shares of XYZ @ $45/share (Proceeds = $4,500).

- Initial Loss = $500.

- July 25th: Buy 100 shares of XYZ @ $46/share (Replacement purchase within 30 days).

Result:

- The $500 loss on the July 10th sale is disallowed for the current tax year because you bought XYZ back on July 25th.

- The disallowed loss of $500 is added to the cost basis of the July 25th purchase.

- Your new cost basis for the shares bought on July 25th is $4,600 (purchase cost) + $500 (disallowed loss) = $5,100, or **$51 per share**.

You won’t recognize that original $500 loss until you sell these new shares (acquired July 25th) and stay out of XYZ for at least 31 days.

“Substantially Identical”: What Does It Really Mean?

This is another fuzzy area. What exactly counts as “substantially identical”?

- Same Stock: Selling AAPL stock at a loss and buying AAPL stock back? Clearly identical.

- Options on the Same Stock: Selling AAPL stock at a loss and buying AAPL call options (or selling AAPL in-the-money put options) within the window? The IRS considers this substantially identical and will trigger the rule.

- Bonds of the Same Issuer: Bonds from the same company are generally considered identical if they have similar maturity dates and coupon rates. Big differences might make them non-identical, but caution is needed.

- Different Share Classes? Selling Class A shares at a loss and buying Class B shares of the same company? Usually considered substantially identical if the classes have similar rights.

- Similar ETFs? (The Gray Area): This is where it gets tricky. Selling SPY (an S&P 500 ETF) at a loss and immediately buying IVV (another S&P 500 ETF from a different provider)? Technically, they aren’t the exact same security. However, the IRS hasn’t given definitive guidance. Many tax professionals advise caution, as the IRS could argue they are substantially identical because they track the same index and have nearly identical performance. Buying an ETF tracking a different index (like QQQ for Nasdaq 100) is generally considered safe.

Common Wash Sale Traps for Active Traders

Active traders are prime candidates for wash sale penalties due to frequent buying and selling. Here are the traps to watch out for:

Trap 1: Wash Sales Across Multiple Accounts (The IRA Nightmare)

This is the absolute worst-case scenario. The wash sale rule applies across all accounts owned by you or your spouse. This includes taxable brokerage accounts, joint accounts, and Individual Retirement Accounts (IRAs).

- Scenario: You sell MSFT at a $1,000 loss in your taxable account. Five days later, you buy MSFT in your Roth IRA.

- Result: The $1,000 loss in your taxable account is disallowed.

- The Nightmare: Because you cannot adjust the cost basis of assets inside an IRA, that $1,000 loss permanently disappears. You never get a tax benefit for it. Ouch.

Trap 2: Dividend Reinvestment Plans (DRIPs)

If you sell shares of a stock at a loss but are enrolled in a DRIP for that same stock, an automatic dividend reinvestment purchase within the 61-day window can trigger a wash sale. Consider turning off DRIPs temporarily if you plan to harvest losses.

Trap 3: Options Assignments and Exercises

Options add complexity. Being assigned on a short put (forced to buy stock) or exercising a long call (choosing to buy stock) counts as acquiring the stock. If this happens within the 61-day window of selling the same stock at a loss, it can trigger a wash sale.

Trap 4: Year-End Transactions (December Danger Zone)

Wash sales occurring late in December are particularly painful. If you sell at a loss on December 15th and buy back on January 5th (within 30 days), the loss from December is disallowed for that tax year. You have to wait until you sell the new shares in the following year (or later) to potentially recognize it. This can mess up your tax planning if you were counting on those losses.

Does the Wash Sale Rule Apply to Cryptocurrency? (2025 Status)

Historically, the tax treatment of cryptocurrency regarding wash sales has been different from securities. Because the IRS often classified crypto as “property” rather than a “security,” the wash sale rule technically didn’t apply. This meant you could sell Bitcoin at a loss and buy it back immediately while still claiming the loss.

However, tax laws and IRS interpretations evolve rapidly, especially concerning digital assets.

CRITICAL NOTE FOR 2025 TAXES: You MUST verify the current IRS stance or any new legislation regarding the application of the wash sale rule to cryptocurrencies for the 2025 tax year. Regulations may have changed or been clarified. Do not assume the historical treatment still applies without consulting a qualified tax professional or checking the latest official IRS guidance.

How to Avoid or Mitigate the Wash Sale Rule

While frustrating, the wash sale rule isn’t impossible to manage.

Strategy 1: Wait 31 Days Before Repurchasing

The simplest way? If you sell a security at a loss, just wait 31 full days before buying it back in any account. This puts you outside the 61-day window.

Strategy 2: Buy a Similar but Not Identical Security

If you want to maintain exposure to a sector after selling for a loss, buy a security that is similar but not “substantially identical.” For example:

- Sell Stock A in the tech sector, buy Stock B in the tech sector.

- Sell SPY (S&P 500 ETF), buy QQQ (Nasdaq 100 ETF).

- Sell SPY (S&P 500 ETF), buy VOO (Vanguard S&P 500 ETF) – Caution: This is the gray area, consult a tax pro.

Strategy 3: The Ultimate Fix – Elect Mark-to-Market (MTM)

For traders who qualify for Trader Tax Status (TTS), the most definitive solution is to make the Section 475(f) Mark-to-Market (MTM) election. As confirmed by the IRS, this election changes your trading gains/losses to ordinary income/loss and exempts you from the wash sale rule for the securities covered by the election.

Learn how MTM Accounting Solves This

Record Keeping and Broker Reporting (Form 1099-B)

Your broker is required to track and report wash sales within a single account on your annual Form 1099-B. They will show the disallowed loss amount and the adjusted cost basis.

However, brokers do NOT track wash sales across different accounts (e.g., between your account and your spouse’s, or between your taxable account and your IRA). You are responsible for identifying and correctly reporting these cross-account wash sales. This requires meticulous record-keeping if you trade the same securities in multiple places.

Our Team’s Verdict: Don’t Let Wash Sales Ambush You

The wash sale rule is a significant hurdle, especially for active day traders. The potential for disallowed losses and phantom income is real and costly.

Understanding the 61-day window, the “substantially identical” definition, and particularly the cross-account IRA trap is crucial for basic tax awareness. While strategies like waiting 31 days or swapping securities can help, they hinder trading flexibility.

For serious traders who qualify for TTS, electing MTM is the only way to truly eliminate the wash sale burden and trade freely without this tax headache hanging over every transaction. It’s a key component of a professional trading tax strategy.

- Wash sales are a key part of our Ultimate Guide to Day Trading Taxes.

- Qualifying for Trader Tax Status is the first step towards MTM.

- This is a critical tax topic for our Beginner Awareness guide.

- Wash sales add hidden costs, detailed in Understanding Brokerage Costs.

Frequently Asked Questions (FAQ) About the Wash Sale Rule

What exactly triggers the wash sale rule?

Quick Answer: Selling a security at a loss and buying a “substantially identical” one within 30 days before or after the sale.

The rule is triggered by the combination of realizing a loss and re-establishing your position in the same or a very similar security within the 61-day window (30 days prior, sale date, 30 days after). This includes buying the stock back, buying call options, or selling in-the-money puts on the same stock.

Key Takeaway: Both the loss sale and the repurchase within the specific timeframe are necessary to trigger the rule.

How long do I have to wait to avoid a wash sale?

Quick Answer: You must wait at least 31 full days after the date of the loss sale before repurchasing.

The wash sale window extends 30 days after the date of the sale where you incurred a loss. To be completely outside this window, you need to wait until the 31st day (or later) following the sale before acquiring a substantially identical security in any of your accounts.

Key Takeaway: Counting 31 days after the sale date is the simplest way to ensure you avoid the rule.

Does the wash sale rule apply if I buy back in a different account?

Quick Answer: Yes, absolutely. It applies across all accounts owned by you and your spouse, including IRAs.

The IRS considers all your accounts (individual taxable, joint taxable, traditional IRA, Roth IRA) as one entity for the wash sale rule. Selling stock at a loss in your brokerage account and buying it back in your Roth IRA within 30 days will trigger the rule, and the loss is permanently disallowed because IRA basis cannot be adjusted.

Key Takeaway: This cross-account application, especially with IRAs, is one of the most dangerous and costly aspects of the rule.

What happens if I have a wash sale?

Quick Answer: The loss on the sale is disallowed for the current tax year, and it gets added to the cost basis of the replacement shares.

You cannot deduct the loss immediately. Instead, the amount of the disallowed loss increases the purchase price (cost basis) of the substantially identical securities you acquired within the 61-day window. This effectively defers the tax benefit of that loss until you sell the new shares (without triggering another wash sale).

Key Takeaway: The loss isn’t gone forever (unless repurchased in an IRA), but its recognition is postponed.

Can I avoid the wash sale rule by buying a similar ETF?

Quick Answer: Maybe, but it’s a gray area and risky. Buying an ETF tracking a different index is safer.

Selling SPY (S&P 500) and buying QQQ (Nasdaq 100) is generally fine. Selling SPY and buying IVV (another S&P 500 ETF) is riskier. While technically different securities, the IRS could argue they are “substantially identical” due to tracking the same index and having nearly identical performance. There’s no definitive IRS ruling.

Key Takeaway: Consult a tax professional. Swapping to an ETF with clearly different underlying holdings or index is the safest approach.

Does the wash sale rule apply to options?

Quick Answer: Yes. Acquiring options on the stock you sold at a loss can trigger the rule.

If you sell stock XYZ at a loss, buying XYZ call options (a contract to buy) or selling XYZ in-the-money put options (creating an obligation to potentially buy) within the 61-day window is treated by the IRS as acquiring a “substantially identical” interest, triggering the wash sale rule.

Key Takeaway: Options traders need to be just as careful about wash sales as stock traders.

Does the wash sale rule apply to cryptocurrency in 2025?

Quick Answer: This requires verification. Historically, it often hasn’t, but IRS rules may have changed.

In the past, the IRS generally classified cryptocurrencies like Bitcoin as “property,” not “securities.” The wash sale rule in Section 1091 of the tax code specifically mentions “stock or securities.” Therefore, many tax professionals interpreted that the rule didn’t apply to crypto. However, the IRS has increased scrutiny on digital assets, and new regulations or legislation might have specifically included cryptocurrencies under wash sale rules or similar provisions for the 2025 tax year.

Key Takeaway: Do not assume the old rules apply. Verify the current IRS position for 2025 with official sources or a qualified tax advisor before trading crypto based on wash sale assumptions.

How does the wash sale rule affect day traders?

Quick Answer: It’s a major problem, often creating large disallowed losses and potential “phantom income” (taxable income despite overall losses).

Day traders frequently buy and sell the same stocks multiple times a day or week. This high frequency makes it extremely easy to trigger wash sales repeatedly. Losses get disallowed and pushed onto the basis of new shares, which are then quickly sold, potentially triggering another wash sale. This chain reaction can defer losses indefinitely or until year-end, leading to a large tax bill that doesn’t reflect the trader’s actual net profit or loss.

Key Takeaway: The wash sale rule is one of the biggest tax hurdles for active stock and options traders who haven’t elected MTM

Article Sources

- IRS Publication 550 – Investment Income and Expenses

- Investopedia – Wash Sale Rule

- Fidelity/Schwab Learning Centers: Brokerage sources are reliable for cross-account/IRA trap explanations)

- IRS Topic No. 429 – Traders in Securities

- Specialized Tax Websites (e.g., Green Trader Tax)

{kind=link}